Math has spoken: The best ways to repay your federal student debt

Student loan repayment has never been simple. It’s hard to pay attention to all the repayment plans, finance terms, and approaches to debt repayment. 😴

As a team of math and finance experts, we’re constantly researching better ways to accelerate you to $0 student debt! We found a study that has determined the repayment strategies that save federal student loan borrowers the most money.

What’s the best plan of attack? Make more payments early on and in special circumstances sign up for an incoming driven repayment plan later on.

Taking note of these strategies could save you thousands of dollars over the life of your federal student loans.

Let’s dig in.

A note before we start: the study assumes borrowers are paying their loans with only their own money (they’re not signed up with Dolr yet 😉). The study is solving to save borrowers the most money, not necessarily get them to $0 debt in the least amount of time.

We’ve solved for both by finding you extra cash for your student loans from where you work, live, and shop. When extra money to your loans doesn’t cost you anything, maximizing your payments with Dolr is the best strategy for you to save time and money.

Repayment plans and taxes make things complicated

When money is borrowed, the lender charges extra money on top of what is borrowed to compensate for the risks of lending the money. That extra money is interest.

Interest grows with time, so general consensus says to repay loans as quickly as possible.

Paying more towards your loans is never a bad idea, but there are other factors at play in the case of federal student loans. Namely, the availability of income-driven repayment plans and the taxes that go with them.

Income-driven repayment plans

Income-driven repayment (IDR) plans are available for eligible federal student loan borrowers.

These plans set your minimum monthly payments to an amount that is intended to be affordable based on income and family size.

The lower the income and greater the number of dependents, the smaller the minimum monthly payment can be.

Less up due up front, more owed at the end

Interest continues to accrue under IDR plans. You save cash in the short-term because your monthly payment is lower, but your outstanding balance is left to grow to a much larger number than if you were making maximum payments.

Pro tip: Borrowers must recertify their income each year under an IDR plan; failure to do so will result in any outstanding interest being capitalized. Beware!

Under the current IDR plan options, any remaining loan balance is forgiven if your federal student loans aren't fully repaid at the end of the repayment period.

Here’s the catch: you must pay taxes on the amount that is forgiven.

This creates a unique situation. If the amount left to be forgiven is too high, the tax burden will outweigh your short-term savings from a lower monthly payment under an IDR plan.

This is the problem the study sought to solve, by answering a few questions:

- When does it make sense to simply maximize your payments and ignore IDR?

- If IDR plans are the right path, what is the optimal point to enroll?

Life without Dolr

Reminder: borrowers receiving free extra cash for their student loan payments through Dolr are already on the fastest path to $0 student debt. The findings of the study apply most directly to those working hard to fund their loan repayment themselves.

According to the study, the best approach depends on your interest rate, the tax rate, and how much time is left until your balance is forgiven under an IDR.

In general:

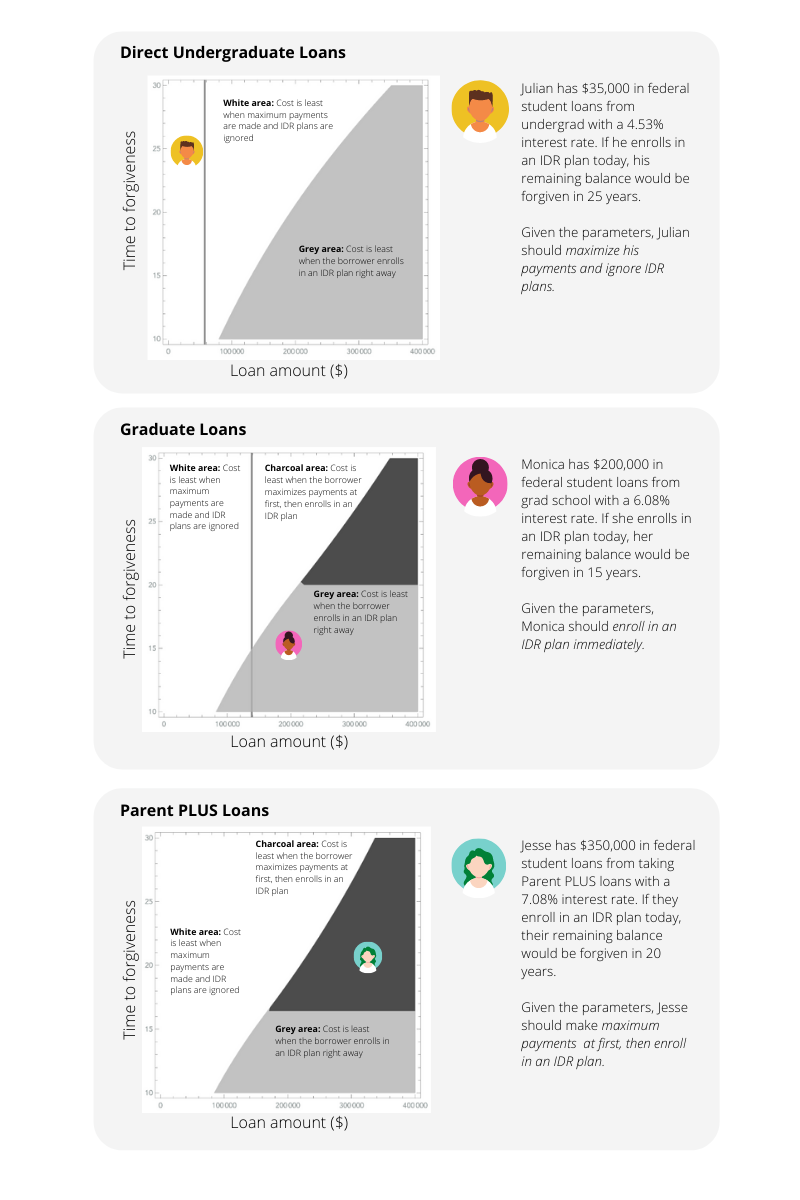

- For small loan balances: Paying off your loan as early as possible through maximum payments and ignoring IDR plans is the best strategy to minimize costs.

- For large loan balances: Taking advantage of IDR plans and either (1) enrolling in one right away or (2) making maximum payments to a point, then enrolling in an IDR plan are the two best strategies to minimize costs.

A few examples:

Life with Dolr

We’ve hinted at this a bit - Dolr is the optimal approach to repaying your student loans. We set out to find YOU more cash for your student loans so that YOU can accelerate to $0 student debt at no additional cost to YOU.

That’s why we can say it’s the best approach.

By getting other sources of cash sent to your student loans (your employer, your credit card rewards, the places you shop, etc.), the formula gets much simpler.

Get more money to your student loans with Dolr to get out of debt faster and save big on your student loans.

Keep accelerating to $0 student debt!

Keep up the good work. If you’re wondering where you can find additional sources of cash for your student loans, create a free account with Dolr. 😊

Subscribe to our blog or follow us on social for more tips on how to accelerate to $0 student debt.